9 Student Loan Repayment Plans Explained (Federal Options Guide)

Last updated on April 7th, 2026 at 12:03 am

If you’re trying to understand how student loan repayment plans work, you’re not alone.

I didn’t understand them either when I graduated in 2013 with a Master’s in Accounting and $26,000 in student loan debt.

Like many graduates, I remember signing a stack of paperwork, attending an exit interview, and being told I had a six-month grace period before repayment would begin.

Six months later, the bill arrived; $294 per month and my repayment journey officially started.

At the time, a student loan representative told me I was enrolled in the standard repayment plan. I followed that plan and eventually paid off the full $26,000.

What I didn’t realize then was that multiple repayment options existed, each with very different rules, timelines, and potential outcomes.

Considering Americans now hold over $1.6 trillion in student loan debt across more than 45 million borrowers, understanding these options matters more than ever.

In this guide, we’ll break down the major federal student loan repayment plans, how they work, and how to decide which one may make the most sense for your situation.

Before we break down each repayment plan, it helps to understand what your monthly payment could actually look like based on your loan balance and income. Use the Student Loan Repayment Calculator to estimate your monthly payment.

Student Loan Repayment Plans & How They Work.

When it’s time to repay your student loans, it’s important to know what student loan repayment plans are available so you can make an informed decision that works for you.

It is important to note that these student loan repayment plans discussed here only apply to federal student loans.

1. Standard Student Loan Repayment Plan:

The Standard Repayment Plan is the most common federal student loan repayment option and is typically the default plan assigned by loan servicers.

Under this plan, your loan balance is divided into fixed monthly payments over 10 years (120 months). Because the repayment period is shorter than many other plans, the monthly payment amount is usually higher.

However, the trade-off is that you pay less interest over time, which means the Standard Repayment Plan is often the least expensive option overall if you can comfortably afford the monthly payment.

If you do not select a different repayment plan after your grace period ends, your loan servicer will generally place you on the Standard Repayment Plan automatically.

Loans eligible for the Standard Repayment Plan include:

- Direct Subsidized Loans

- Direct Unsubsidized Loans

- Direct PLUS Loans

- Direct Consolidation Loans

- FFEL PLUS Loans

- FFEL Consolidation Loans

- Subsidized Federal Stafford Loans

- Unsubsidized Federal Stafford Loans

If your loan type is not listed above, it may not qualify for this repayment plan.

2. Graduated Student Loan Repayment Plan:

The Graduated Student Loan Repayment Plan is designed for borrowers who expect their income to increase over time.

Under this plan, your monthly payments start lower at the beginning and gradually increase as time goes on. Payments typically increase every two years, which is why it’s called the graduated repayment plan.

The idea behind this option is simple: many borrowers start their careers with lower salaries and expect their earnings to grow as they gain experience and move into more senior roles.

For most federal loans, the repayment period under the Graduated Plan is 10 years. However, if you have consolidated loans, the repayment period can extend up to 30 years depending on the loan balance.

Because payments start lower and increase over time, borrowers may end up paying more in total interest compared to the Standard Repayment Plan.

Loans eligible for the Graduated Repayment Plan include:

- Direct Subsidized Loans

- Direct Unsubsidized Loans

- Direct PLUS Loans

- Direct Consolidation Loans

- FFEL PLUS Loans

- FFEL Consolidation Loans

- Subsidized Federal Stafford Loans

- Unsubsidized Federal Stafford Loans

If your loan type is not listed above, it may not qualify for this repayment option.

3. The Extended Student Loan Repayment Plan:

If you need more time to repay your federal student loans, the Extended Student Loan Repayment Plan may be an option worth considering.

Under this plan, borrowers can stretch their repayment term up to 25 years, which can significantly lower the monthly payment compared to the Standard Repayment Plan.

However, to qualify, you must have more than $30,000 in outstanding federal student loan debt.

Borrowers under the Extended Repayment Plan can choose between:

- Fixed monthly payments, where the payment amount stays the same throughout the life of the loan, or

- Graduated payments, where the payment starts lower and increases over time.

While extending the repayment timeline can make monthly payments more manageable, it also means you may pay more interest over the life of the loan.

Loans eligible for the Extended Repayment Plan include:

- Direct Subsidized Loans

- Direct Unsubsidized Loans

- Direct PLUS Loans

- Direct Consolidation Loans

- FFEL PLUS Loans

- FFEL Consolidation Loans

- Subsidized Federal Stafford Loans

- Unsubsidized Federal Stafford Loans

Borrowers must have more than $30,000 in outstanding federal student loan debt to qualify for this repayment plan.

If your loan type is not listed above, it may not qualify for this repayment option.

4. The Income Sensitive Student Loan Repayment Plan:

The Income-Sensitive Repayment Plan (ISR) is a repayment option available to borrowers with loans under the Federal Family Education Loan (FFEL) Program.

Under this plan, your monthly payment is based on your income, which can help make payments more manageable if your earnings fluctuate or are relatively low.

Unlike some other repayment plans, the payment amount is recalculated each year based on your income, meaning your monthly payment may increase or decrease over time.

The repayment term for the Income-Sensitive Repayment Plan is up to 10 years.

It is important to note that this plan only applies to FFEL Program loans and is not available for Direct Loans issued through the U.S. Department of Education.

Loans eligible for the Income-Sensitive Repayment Plan include:

- FFEL PLUS Loans

- FFEL Consolidation Loans

- Subsidized Federal Stafford Loans (FFEL Program)

- Unsubsidized Federal Stafford Loans (FFEL Program)

If your loan type is not listed above, it may not qualify for this repayment option. .

5. Income-Driven Student Loan Repayment Plans (IDR):

Income-Driven Repayment (IDR) plans are designed to make federal student loan payments more affordable by tying your monthly payment to your income and family size.

Instead of paying a fixed amount based strictly on your loan balance, IDR plans calculate your payment using a percentage of your discretionary income, which is based on your Adjusted Gross Income (AGI) and household size.

Because payments are based on income, these plans can be especially helpful for borrowers who have lower earnings relative to their loan balance.

Income-Driven Repayment plans are also commonly used by borrowers pursuing student loan forgiveness, since any remaining balance may be forgiven after a certain number of qualifying payments depending on the specific plan.

However, Income-Driven Repayment is considered the most complex category of student loan repayment options because it includes several different plans, each with its own eligibility rules, repayment timelines, and payment calculations.

The main Income-Driven Repayment plans include:

- Income-Based Repayment (IBR)

- Pay As You Earn (PAYE)

- Income-Contingent Repayment (ICR)

- Saving on a Valuable Education (SAVE) which replaced the Revised Pay As You Earn (REPAYE) plan for many borrowers

Income-driven repayment plans adjust your monthly payment based on your income; but the actual number can vary significantly. See your loan payment breakdown.

In the sections below, we’ll break down each of these repayment plans and explain how they work, who qualifies, and how payments are calculated.

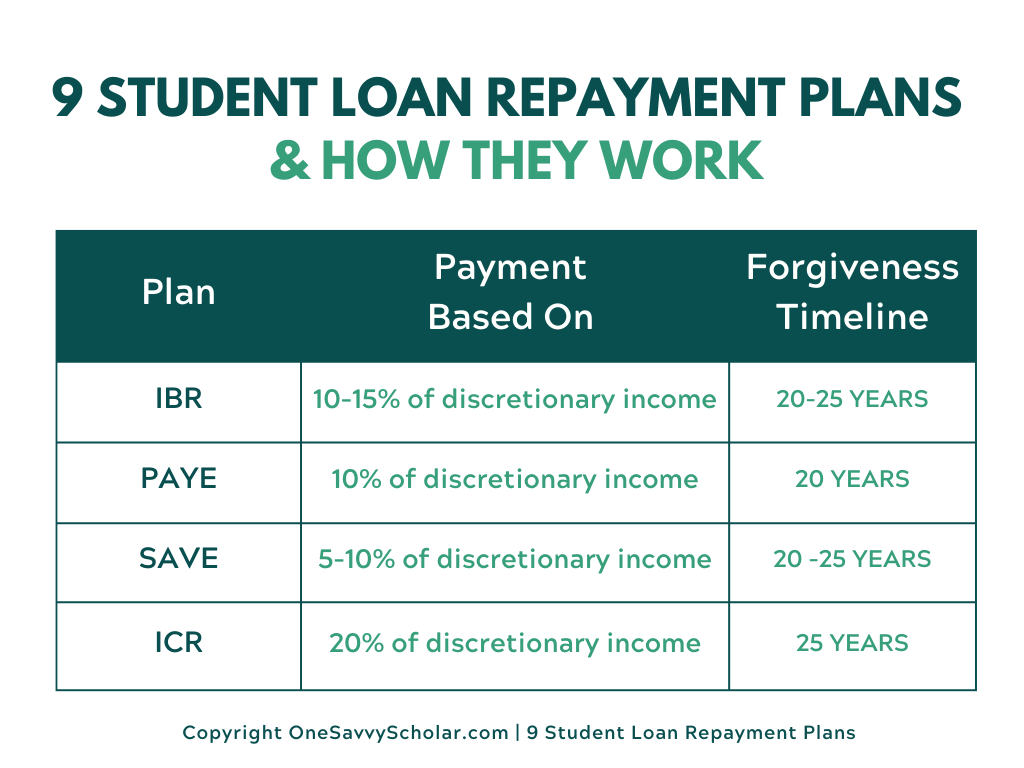

5a. Income-Based Student Loan Repayment Plan (IBR Plan)

The Income-Based Repayment (IBR) Plan is one of the original income-driven repayment options designed to make federal student loan payments more manageable.

Under this plan, your monthly payment is based on a percentage of your discretionary income and your family size.

For most borrowers, payments are calculated as:

- 10% of discretionary income for borrowers who took out loans after July 1, 2014, or

- 15% of discretionary income for borrowers who took out loans before July 1, 2014

To qualify for the IBR Plan, you must demonstrate a partial financial hardship, meaning your payment under the IBR formula would be lower than what you would pay under the Standard Repayment Plan.

Depending on when you borrowed your loans, any remaining balance may be eligible for forgiveness after 20 or 25 years of qualifying payments.

Loans eligible for the Income-Based Repayment Plan include:

- Direct Subsidized Loans

- Direct Unsubsidized Loans

- Direct PLUS Loans made to graduate or professional students

- Direct Consolidation Loans that did not repay Parent PLUS loans

- Subsidized Federal Stafford Loans (FFEL Program)

- Unsubsidized Federal Stafford Loans (FFEL Program)

- FFEL PLUS Loans made to graduate or professional students

- FFEL Consolidation Loans that did not repay Parent PLUS loans

Loans that may qualify if consolidated into a Direct Consolidation Loan:

-

Federal Perkins Loans

Parent PLUS loans do not qualify for the Income-Based Repayment Plan, even if consolidated.

If your loan type is not listed above, it may not be eligible for this repayment plan.

Revised Pay As You Earn Repayment Plan (REPAYE Plan)

The Revised Pay As You Earn (REPAYE) Plan was an income-driven repayment option that calculated monthly student loan payments based on 10% of a borrower’s discretionary income.

Under REPAYE, borrowers could qualify for student loan forgiveness after making qualifying payments for 20 or 25 years, depending on the type of loan:

- 20 years for undergraduate loans

- 25 years for graduate or professional school loans

Unlike some other income-driven repayment plans, REPAYE did not require borrowers to demonstrate partial financial hardship in order to qualify.

It is important to note that the REPAYE plan has largely been replaced by the SAVE Plan (Saving on a Valuable Education), which offers updated payment calculations and additional borrower protections.

Loans eligible for the REPAYE Plan included:

- Direct Subsidized Loans

- Direct Unsubsidized Loans

- Direct PLUS Loans made to graduate or professional students

- Direct Consolidation Loans that did not repay Parent PLUS loans

Loans that could qualify if consolidated into a Direct Consolidation Loan:

- Subsidized Federal Stafford Loans (FFEL Program)

- Unsubsidized Federal Stafford Loans (FFEL Program)

- FFEL PLUS Loans made to graduate or professional students

- FFEL Consolidation Loans that did not repay Parent PLUS loans

- Federal Perkins Loans

Parent PLUS loans do not qualify for REPAYE, even if consolidated.

If your loan type is not listed above, it may not be eligible for this repayment plan.

5b. Saving on a Valuable Education Repayment Plan (SAVE Plan)

The Saving on a Valuable Education (SAVE) Plan is one of the newest income-driven repayment options for federal student loan borrowers. This plan replaced the Revised Pay As You Earn (REPAYE) Plan and was designed to make student loan payments more affordable.

Under the SAVE Plan, your monthly payment is calculated as a percentage of your discretionary income, which is based on your adjusted gross income (AGI) and family size.

For many borrowers, monthly payments may be as low as:

- 5% of discretionary income for undergraduate loans

- 10% of discretionary income for graduate school loans

If a borrower has both undergraduate and graduate loans, the payment percentage is weighted based on the loan balance.

One of the key benefits of the SAVE Plan is that it increases the income threshold used to calculate discretionary income, which may lower monthly payments for many borrowers.

In addition, if your monthly payment under SAVE does not fully cover the interest that accrues on your loan, the government may cover the remaining unpaid interest, preventing your loan balance from growing due to unpaid interest.

Borrowers may qualify for loan forgiveness after making qualifying payments for 20 or 25 years, depending on the type of loan.

Loans eligible for the SAVE Plan include:

- Direct Subsidized Loans

- Direct Unsubsidized Loans

- Direct PLUS Loans made to graduate or professional students

- Direct Consolidation Loans that did not repay Parent PLUS loans

Loans that may qualify if consolidated into a Direct Consolidation Loan:

- Subsidized Federal Stafford Loans (FFEL Program)

- Unsubsidized Federal Stafford Loans (FFEL Program)

- FFEL PLUS Loans made to graduate or professional students

- FFEL Consolidation Loans that did not repay Parent PLUS loans

- Federal Perkins Loans

Parent PLUS loans do not qualify for the SAVE Plan, even if consolidated.

If your loan type is not listed above, it may not qualify for this repayment option.

Update: The SAVE Plan (Saving on a Valuable Education) was introduced as a more affordable income-driven repayment option. However, due to recent legal and policy changes, the plan is no longer being actively implemented, and borrowers may be required to choose an alternative repayment plan by July 1, 2026.

Borrowers should review current options and confirm their eligibility with the U.S. Department of Education, as repayment programs can change over time.

5c. Income-Contingent Repayment Plan (ICR Plan)

The Income-Contingent Repayment (ICR) Plan is one of the oldest income-driven repayment options available for federal student loans.

Under this plan, your monthly payment is calculated as the lesser of:

- 20% of your discretionary income, or

- the amount you would pay on a fixed 12-year repayment plan adjusted for your income

Because payments are tied to income, the amount you pay may increase or decrease over time depending on your earnings.

Borrowers enrolled in the ICR Plan may qualify for loan forgiveness after 25 years of qualifying payments.

One unique feature of the ICR Plan is that Parent PLUS loan borrowers may access this plan if they consolidate their loans into a Direct Consolidation Loan.

Loans eligible for the Income-Contingent Repayment Plan include:

- Direct Subsidized Loans

- Direct Unsubsidized Loans

- Direct PLUS Loans made to graduate or professional students

- Direct Consolidation Loans that did not repay Parent PLUS loans

- Direct Consolidation Loans that repaid Parent PLUS loans

Loans that may qualify if consolidated into a Direct Consolidation Loan:

- Direct PLUS Loans made to parents

- Subsidized Federal Stafford Loans (FFEL Program)

- Unsubsidized Federal Stafford Loans (FFEL Program)

- FFEL PLUS Loans made to graduate or professional students

- FFEL PLUS Loans made to parents

- FFEL Consolidation Loans that did not repay Parent PLUS loans

- FFEL Consolidation Loans that repaid Parent PLUS loans

- Federal Perkins Loans

If your loan type is not listed above, it may not qualify for this repayment option.

5d. Pay As You Earn Repayment Plan (PAYE Plan)

The Pay As You Earn (PAYE) Plan is an income-driven repayment option designed to make federal student loan payments more affordable.

Under the PAYE Plan, your monthly payment is generally limited to 10% of your discretionary income, based on your adjusted gross income (AGI) and family size.

To qualify for the PAYE Plan, borrowers must demonstrate a partial financial hardship, meaning the calculated PAYE payment must be lower than the payment under the Standard Repayment Plan.

Borrowers enrolled in PAYE may qualify for student loan forgiveness after 20 years of qualifying payments.

It is also important to note that the PAYE Plan is only available to “new borrowers.” This generally means you must not have had outstanding federal student loans before October 1, 2007, and you must have received a Direct Loan on or after October 1, 2011.

Loans eligible for the PAYE Plan include:

- Direct Subsidized Loans

- Direct Unsubsidized Loans

- Direct PLUS Loans made to graduate or professional students

- Direct Consolidation Loans that did not repay Parent PLUS loans

Loans that may qualify if consolidated into a Direct Consolidation Loan:

- FFEL PLUS Loans made to graduate or professional students

- FFEL Consolidation Loans that did not repay Parent PLUS loans

- Federal Perkins Loans

- Subsidized Federal Stafford Loans (FFEL Program)

- Unsubsidized Federal Stafford Loans (FFEL Program)

Parent PLUS loans do not qualify for the PAYE Plan, even if consolidated.

If your loan type is not listed above, it may not qualify for this repayment option.

Frequently Asked Questions About Student Loan Repayment Plans

1. How do I know which repayment plan is right for me?

The best plan isn’t the one with the lowest monthly payment—it’s the one that fits your real life. If your income is unstable or you’re a working student, income-driven plans can give you breathing room.

But if your goal is to get out of debt faster and you can afford higher payments, a standard plan may cost you less over time.

2. Can I switch repayment plans later?

Yes; and most people do. Your financial situation will change, and your repayment plan should change with it. The key is not to “set it and forget it,” but to check in at least once a year and adjust if needed.

3. Why did my monthly payment increase?

This usually happens if:

- your income increased (on income-driven plans)

- you missed recertification deadlines

- or your loan moved into a different repayment structure

It’s not random but it feels that way if you’re not aware of the rules behind your plan.

4. What’s the difference between income-driven repayment (IDR) and other plans?

Income-driven plans adjust your monthly payment based on what you earn, not just what you owe. Traditional plans focus on paying off the loan in a fixed time. IDR gives flexibility; but often stretches the repayment timeline longer.

5. Is the SAVE Plan still available?

The SAVE Plan is no longer being actively implemented, and many borrowers are expected to transition to other repayment plans. If you were previously enrolled, you should review your current status and prepare to select a new repayment option if required.

6. Will a lower monthly payment save me money?

Not always. Lower payments can mean:

- longer repayment periods

- more interest paid over time

It helps your cash flow today, but may cost more in the long run. That tradeoff is important.

7. What happens if I don’t choose a repayment plan?

You’ll automatically be placed into the standard repayment plan. For many borrowers; especially working students, that payment can feel too high because it doesn’t consider your income.

8. Is loan forgiveness guaranteed under student loan repayment plans?

No. Some plans offer forgiveness after a certain number of years, but there are strict requirements. Missing steps for instance; annual income recertification, can reset your progress without you realizing it.

9. Why is student loan repayment so confusing?

Because the system wasn’t built for simplicity; it was built in layers over time. That’s why two people with similar loans can have completely different payment experiences.

Choosing the right repayment plan isn’t just about understanding your options; it’s about understanding your numbers. Estimate your monthly student loan payment to compare scenarios and find the best plan for your situation.

Final Thoughts:

Most federal student loan borrowers qualify for at least one income-driven repayment plan. Depending on your income and family size, your required monthly payment could even be as low as $0.

However, it’s important to understand that even if your required payment is $0, interest may still accrue on your loan balance depending on the repayment plan.

For borrowers pursuing student loan forgiveness, income-driven repayment plans are often part of the strategy. Just remember that you must recertify your income and family size each year with your loan servicer to remain eligible.

While choosing the right repayment plan can help manage your payments, another strategy many borrowers overlook is employer tuition reimbursement benefits.

Ready to find companies that will help pay for your degree?

Many working students and early-career professionals don’t realize that employer education benefits like tuition reimbursement can reduce the need for future student loans.

I created a database to make it easier to find them without digging through hundreds of websites.

Find Companies That Offer Tuition Reimbursement

The OneSavvyScholar Tuition Reimbursement Database tracks companies that help employees pursue degrees while they work. Inside the database, you'll discover;- Tuition reimbursement amounts

- Waiting periods

- Full-time vs part-time eligibility and much more!