Subsidized vs Unsubsidized Student Loans: What Borrowers Should Know

When I was in graduate school, most of my student loans were unsubsidized federal loans.

Unlike some undergraduate loans, these loans started accruing interest immediately, even while I was still in school.

After graduating, I received a six-month grace period before repayment began. Once that period ended, my first monthly bill arrived: $294 per month.

I started making payments in 2014, and what was supposed to be a 10-year repayment plan ended much sooner.

By 2017, the loan was completely paid off.

Part of the reason I was able to eliminate the debt quickly was because I was working while earning my degree. Between my income and tuition reimbursement benefits, my total loan balance was relatively small compared to the national average.

But many students don’t fully understand the type of federal loan they’re taking out, and that distinction can significantly affect how much they ultimately repay.

Before borrowing, it’s important to understand the difference between subsidized vs. unsubsidized student loans.

What Are Subsidized Student Loans?

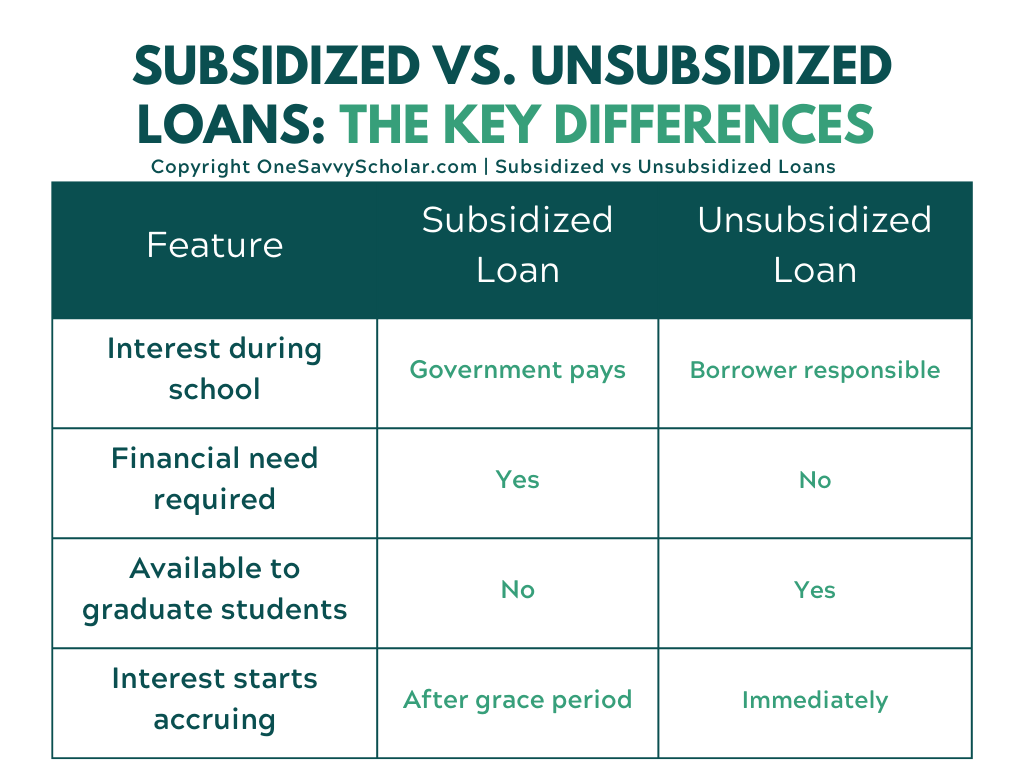

Subsidized loans are federal student loans where the government pays the interest for you during certain periods. These loans are designed primarily for undergraduate students with demonstrated financial need.

Key features of subsidized loans

• Available only to undergraduate students

• Must demonstrate financial need through FAFSA

• Interest does not accrue while you are in school (at least half-time)

• Interest is also covered during the grace period after graduation

• Interest may be covered during certain deferment periods

Because the government covers the interest during school, subsidized loans are generally considered the most favorable type of federal student loan.

This means the balance you borrow is typically the balance you enter repayment with.

What Are Unsubsidized Student Loans?

Unsubsidized loans are federal student loans where interest begins accruing immediately after the loan is disbursed. These loans are available to both undergraduate and graduate students, and they do not require financial need.

Key features of unsubsidized loans

• Available to undergraduate, graduate, and professional students

• No financial need requirement

• Interest begins accruing as soon as the loan is issued

• Borrowers are responsible for all interest charges

Even though payments usually aren’t required while you’re in school, the interest continues accumulating in the background.

If you don’t pay the interest while enrolled, it may be capitalized, meaning it gets added to your principal balance once repayment begins.

Subsidized vs. Unsubsidized Loans: The Key Difference

The main difference comes down to who pays the interest while you’re in school. For many graduate students, unsubsidized loans are the only federal option available.

That’s why it’s especially important to understand how interest works before borrowing.

Why Working Students Sometimes Borrow Less

One advantage many working students have is the ability to reduce borrowing altogether. Students who work while earning their degrees may be able to:

• Pay some tuition out-of-pocket

• Take fewer loans

• Use tuition reimbursement programs offered by companies

• Make loan payments while still in school

All of these strategies can dramatically reduce the total interest paid over time.

In my case, combining work with school helped keep my overall loan balance manageable, which made it possible to eliminate the debt in just a few years.

The Bottom Line

Subsidized and unsubsidized loans may both come from the federal government, but they work very differently.

Subsidized loans provide a major advantage by covering interest while you’re in school, while unsubsidized loans require borrowers to take on that cost themselves.

For students trying to minimize debt, the best strategy is often a combination of:

• Borrowing only what is necessary

• Understanding how interest works

• Looking for companies that help pay for education

• Creating a plan to repay loans as quickly as possible

For many working students, the goal isn’t just graduating; it’s graduating without carrying student debt for decades afterward.

Find Companies That Offer Tuition Reimbursement

The OneSavvyScholar Tuition Reimbursement Database tracks companies that help employees pursue degrees while they work. Inside the database, you'll discover;- Tuition reimbursement amounts

- Waiting periods

- Full-time vs part-time eligibility and much more!

The Working Student Perspective on Student Loans

For students who are working while earning their degrees, student loans often look very different than they do for traditional full-time students.

Many working students are balancing full-time jobs, coursework, and financial responsibilities, which means their borrowing decisions are often shaped by practical realities rather than campus life.

Some working students:

• Attend school part-time

• Pay portions of tuition out of pocket

• Receive tuition reimbursement from the companies they work for

• Borrow smaller loan amounts compared to traditional students

Because of this, their student loan strategy may focus less on borrowing the maximum amount available and more on minimizing debt while progressing toward a degree.

In many cases, working students are trying to do two things at once: build a career and earn a degree at the same time.

That combination can reduce the total amount borrowed and shorten the repayment timeline after graduation.

In my case, working while earning my degree allowed me to keep my loan balance manageable. What began as a standard 10-year repayment plan ended up taking just three years to pay off.

Every student’s situation is different, but understanding how loans work; especially the difference between subsidized and unsubsidized loans can help students make more informed borrowing decisions.

Frequently Asked Questions About Subsidized and Unsubsidized Student Loans

What is the main difference between subsidized and unsubsidized student loans?

The main difference is how interest is handled while you are in school.

With subsidized student loans, the federal government pays the interest while you are enrolled at least half-time and during the grace period after graduation.

With unsubsidized student loans, interest begins accruing as soon as the loan is disbursed, and the borrower is responsible for paying all of it.

Do unsubsidized student loans accrue interest while you’re in school?

Yes. Unsubsidized student loans begin accruing interest immediately after the loan is issued, even while you are still in school.

Although payments are usually not required during enrollment, the interest continues to accumulate. If it isn’t paid during that time, it may be added to the loan balance when repayment begins.

Are subsidized loans available for graduate students?

No. Subsidized federal student loans are only available to undergraduate students who demonstrate financial need. Graduate and professional students typically qualify for unsubsidized loans instead.

Is a subsidized student loan better than an unsubsidized loan?

In most cases, subsidized loans are considered more favorable because the government pays the interest while the borrower is still in school.

This prevents the loan balance from growing before repayment begins.

However, not all students qualify for subsidized loans, and graduate students usually only have access to unsubsidized loans.

Should you pay interest on unsubsidized loans while in school?

If possible, paying the interest while in school can reduce the total cost of the loan.

When interest is not paid during enrollment, it may be capitalized, meaning it gets added to the principal balance once repayment begins.

Paying even small amounts toward interest during school can prevent the balance from growing over time.

Many working students reduce their loan borrowing by choosing companies that offer tuition reimbursement benefits. You can explore companies that help pay for education inside the OneSavvyScholar database.